Health insurance is the fastest-growing line in Indian insurance. Post-COVID, awareness has jumped — and so has competition between insurers. For agents who specialise here, the opportunity is real: high-value annual premiums, strong renewal cycles, multiple cross-sell levers, and customers who genuinely value the agent who guides them through claims. This guide walks through how Indian agents should approach health insurance as a specialization — product mix, cross-sell strategy, claim handholding, and renewal discipline.

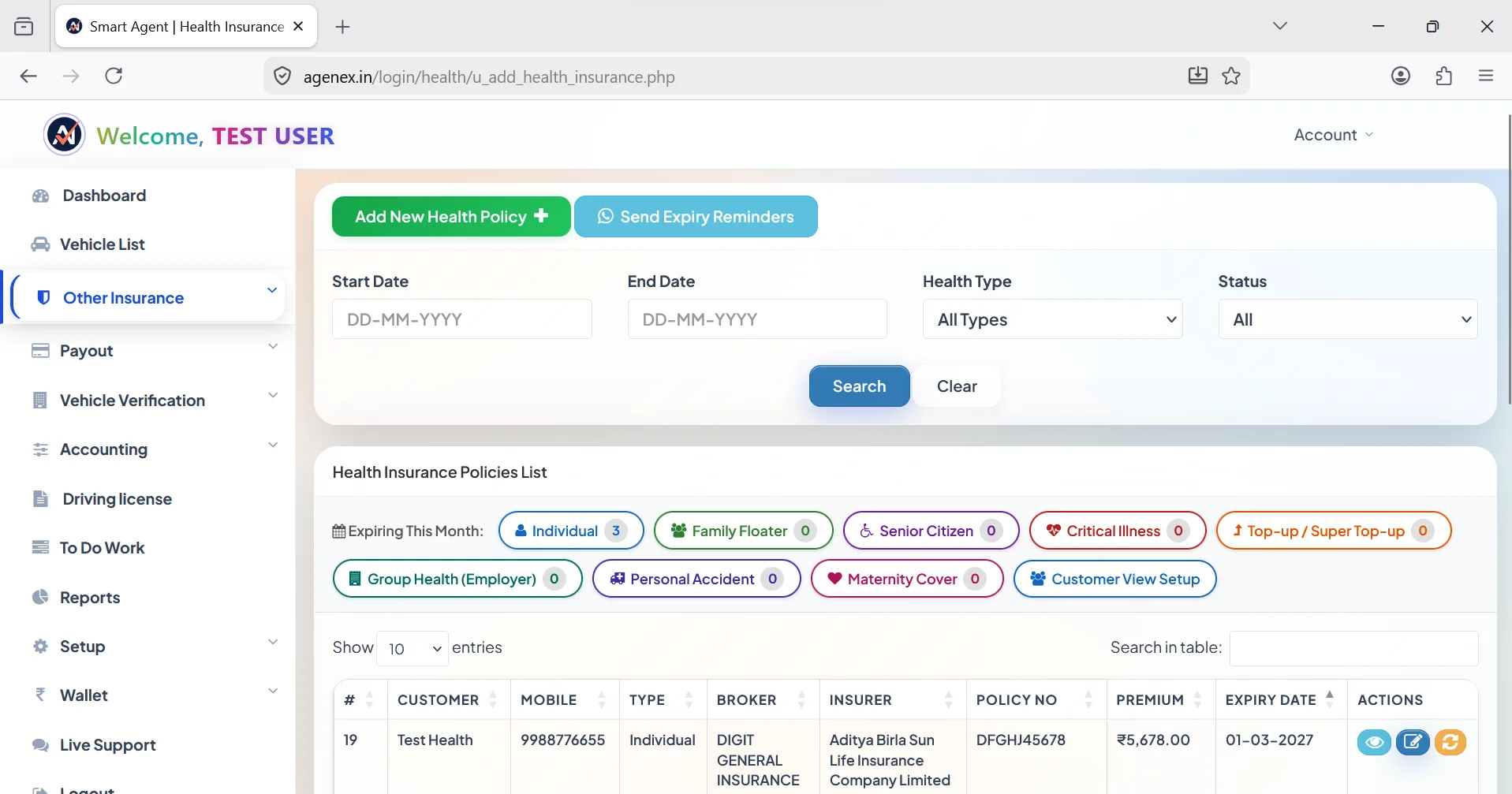

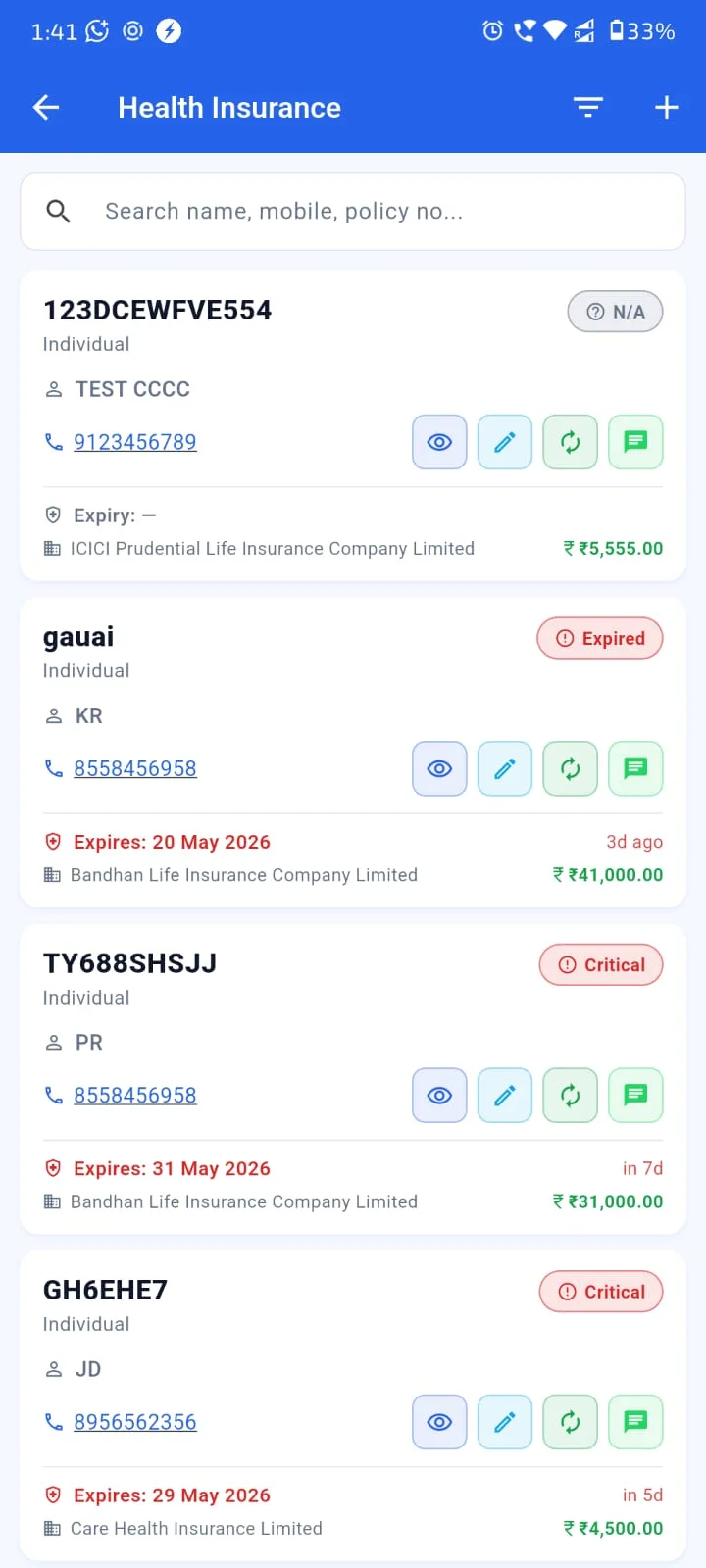

The difference between a struggling health agent and a thriving one usually isn't product knowledge. Both know their products. The difference is workflow — how they track family floaters with multiple insured members, how they remember waiting periods and PED disclosures, how they manage cross-sell timing. A specialized insurance agent app with proper health module support handles all this in the background, so the agent can focus on advice and relationship building. Related: Health Insurance Agent Software, Health Insurance Portfolio Tracker and Health Renewal Management.

Product Categories — Know Your Toolkit

The Indian health insurance market has more product variations than most agents initially appreciate. The major categories:

- Individual indemnity plans: Standard hospitalization cover. The most common starter product. ₹3-25 lakh sum insured ranges.

- Family floater: Single sum insured shared across spouse, kids and sometimes parents. The most popular working-family product.

- Top-up and super top-up: Layered above a base policy. Cheap way to extend coverage to ₹50-100 lakh for senior family members or higher-risk profiles.

- Critical illness riders: Lump-sum payouts on diagnosis. Different from indemnity — useful for catastrophic illness scenarios.

- Hospital cash and OPD plans: Daily cash benefits, outpatient cover. Niche but valuable for specific customer profiles.

- Senior citizen plans: 60+ products with their own underwriting and PED rules.

- Group / employer policies: Sold through corporates. Higher volume, different commission economics.

A working best insurance CRM for agents stores each policy with its specific product type, riders, and sum insured composition — not just a generic "health policy" entry. This level of detail matters at renewal because each product category has its own renewal triggers and conversation points.

Cross-Sell Opportunities — The Health Agent's Real Advantage

Health insurance has more cross-sell levers than any other line of business. A few patterns the best health agents work systematically:

Motor-to-health: Most motor insurance clients in India still don't have adequate health coverage. The annual motor renewal conversation is a natural moment to ask "do you and your family have health cover?" — and offer a floater on the spot. Motor Insurance Agent Software with cross-line visibility makes this conversation seamless.

Sum-insured upgrades: A family that bought ₹5L cover three years ago has outgrown it. Healthcare inflation has been running 12-15% annually. The natural conversation: "your existing policy is good — but let's add a ₹10-20L top-up so a major hospitalization doesn't drain your savings."

Critical illness add-ons: Existing indemnity customers often don't have critical illness riders. One conversation can attach a CI rider that gives you both better client coverage and additional commission.

Parents' coverage: The 35-45 age customer typically has working parents in their 60s who are uninsured or under-insured. Senior citizen plans address this — and the natural cross-sell time is right after the customer's own renewal.

Your client portfolio manage karne wala app should surface these cross-sell opportunities automatically based on each customer's existing policy profile. Insurance lead manage kaise kare for health is fundamentally about timing — the right offer at the right life stage.

Try Agenex Free

Every Agenex feature is included on a free trial — no credit card required. The insurance digital assistant app with cross-line cross-sell suggestions.

Start Free TrialClaim Handling — The Single Biggest Retention Lever

Health claims are emotional. A family is in a hospital — stressed, scared, exhausted. They reach out to their agent. The agent who handholds them through pre-authorization, cashless coordination, document collection and reimbursement processing creates a customer for life. The agent who says "call the insurer directly" loses them at renewal.

The practical workflow: maintain a per-claim record in your insurance policy tracking app — claim reference number, hospital, TPA contact, pre-auth status, documents submitted, payment timeline. When the family calls in distress, you have everything ready. You can WhatsApp them updates instead of making them wait for confused phone calls. This is the kind of attention that turns transactional health customers into multi-decade relationships. Useful related read: Automated Claims Status Tracker.

Renewal Strategy — 30-Day Grace, Strict Discipline

Health insurance has a unique constraint: lapsed policies often reset Pre-Existing Disease (PED) waiting periods. A customer who lapses a 3-year-old policy loses the PED waiting period they've already served — meaning the next policy treats their existing conditions as fresh waiting periods. This is potentially devastating for the customer and an avoidable failure for the agent.

Automated reminders at 30/15/7/1 day pre-expiry are non-negotiable. WhatsApp + SMS + phone call combination for the most critical days. A customer who lets a health policy lapse is a customer who didn't get reminded clearly enough. Your customer renewal reminder software should treat health policies with extra-tight reminder cadence and a grace-period follow-up (day 7 and day 21 after expiry) to recover any policies that slip through. More on this: Automated Renewal Reminder App, WhatsApp Renewal Reminder App and Never Miss A Policy Renewal.

FAQ

Family floater (5L-10L) for young families, individual indemnity for singles in their 20s-30s, super top-ups for upgrade conversations, and critical illness riders as add-ons across all customer segments.

Family floater health. Most motor clients without health cover are open to the conversation if you bring it up during motor renewal. Top-up and critical illness are natural follow-ups once base health cover is in place.

It's the single biggest retention lever. A clean claim experience usually means the customer renews multiple years and brings their family and friends. A poor claim experience loses the customer immediately.

30/15/7/1 day pre-expiry as standard. Health policies justify additional grace-period reminders at day 7 and day 21 post-expiry given the PED waiting period reset risk.

An insurance agency management software with proper health module support — family floater multi-member tracking, sum insured composition, riders, cashless network linkage, and claim status logging. Agenex's health insurance agent software covers all this end-to-end.

Yes — Star, HDFC ERGO, Niva Bupa, Care, Manipal Cigna, Reliance General, ICICI Lombard and others are all pre-loaded with their respective product structures. Useful when comparing options for the same customer.